The World After COVID

The World After Covid-19

When a force is placed on a material, the material stretches or compresses in response to the force. We are all familiar with materials like rubber which stretch very easily. What happens when the stress is removed depends on how far the atoms have been moved. There are broadly two types of deformation:

Elastic deformation - When the stress is removed the material returns to the dimension it had before the load was applied. The deformation is reversible, non-permanent.

Plastic deformation - This occurs when a large stress is applied to a material. The stress is so large that when removed, the material does not spring back to its previous dimension. There is a permanent, irreversible deformation.

The coming days will see similarities to the Great Depression and the financial crisis of 2008 with it’s effect lasting longer than the 2008 crisis since this particular pandemic has far reaching effect than just the financial system. And we’ll see a permanent deformation but a more anti-fragile economy. We don’t know how bad it will get before it gets any better, but throughout our evolutionary stages, we know that we’ll survive this. In the following paragraphs, my goal is to elucidate the effects and aftermath of the pandemic in order for me to make sense of everything that’s happening.

The Slow Realization of The Fragility Of The Economy

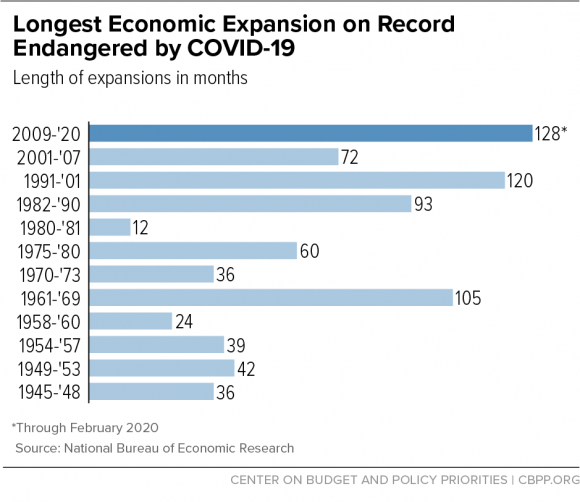

Through February 2020, the U.S. economy had grown for 128 months without any significant decline in economic activity that would mark the beginning of a recession under the criteria used by the National Bureau of Economic Research (NBER), the recognized arbiter of business-cycle dating. The 2009-20 expansion is the longest on record in NBER dating, which goes back to the 1850s.

The Fed as most people would know essentially has has two mandates to maintain stable prices and to achieve “maximum employment.” And the way it does it is by stimulating economic activity in a weak activity by cutting interest rates and by raising interest rates in an overheating economy to control inflation.

Soon after the 2008 crisis, the Fed provided the needed monetary stimulus through the purchase of longer-term assets — a policy known as quantitative easing — to try to lower longer-term interest rates and stimulate interest-sensitive spending more directly. As the interest rates went down, investors continued to enjoy “higher economic growth” as central banks kept on buying financial assets to push economic activity and the inflation up. And though these investors- essentially private equity funds, sovereign wealth funds - got easier access to cheap capital their primary objective was essentially to invest it rather than spend it which is why there hasn’t been any trickle down effect of the economic stimulus to the lower strata of the society.

Because of the continuous bull market in the public markets, more companies didn’t have to make profits or even show a path to profitability while continuing raising money at skyrocketing valuation from venture capital and private equity investment managers, who had unfettered access to dry gunpowder and needed to deploy the capital to make their fees.

And now suddenly with the pandemic, investors are waking up to slow realization of their folly and are asking questions such as:

- Are these things valued fairly or reasonably?

- Is the risk reflected in the price?

- What if the recession hit people so badly that they get 100% of their assets wiped out, which is already happening with major airlines and oil & gas companies on the verge of bankruptcy.

Oil And Gas: Opportunities Following The Carnage (Part 2)

At the same time, pension and healthcare liability payments will increasingly be coming due while many of those who are obligated to pay them don’t have enough money to meet their obligations. Right now many pension funds that have investments that are intended to meet their pension obligations use assumed returns that are agreed to with their regulators. They are typically much higher (around 7%) than the market returns that are built into the pricing and that are likely to be produced

Those who are recipients of these benefits and expecting these commitments to be adhered to are typically teachers and other government employees who are also being squeezed by budget cuts.

With the GDP slated to a hit a 10Y low and the $2 tn stimulus announced by the Government, the Federal Reserve is backing every form of credit now, so it means the US government is now backing every creditor or business and that is a leading indicator of a socialist regime. It will have a massive implication – there will be so much government debt even on the state and local level, that corporate taxes will go up. Since the US government already has massive debts that it owes to foreign governments, this just piles it up more which will most probably have an adverse effect on the USD.

As we will see in the next few paragraphs, the effects of the pandemic is far-reaching and one of the side-effects is deflation! You may ask why?

Well, as spending slows and people lose their jobs, the prices of non-essential things starts to fall, this leads to even lower income for the producers and the workers engaged in that industry. And in turns it leads to further decline in productivity - a circular loop, that’s one reason why controlled inflation is a leading indicator for an economy and the Fed’s targeted 2% inflation before the pandemic hit, which is now impossible.

The Inter-dependency Of The Legos In The Economy

While most people think that they are unaffected by the depression but the effects of recession play out badly in the long term.

Lets do a trace-route of some specific examples

Telecommunications

Most publicly listed telecom companies have a profit margin of 18% with a significant Operational Expenses. Due to the physical infrastructure requirements, they need huge manpower and retail spaces to operate and with the rise of remote work, the network is already at its peak capacity and showing sign of strain and it will eventually lead to greater investment in the underlying infrastructure and further expand the cost bases.

Is the Internet Resilient Enough to Withstand Coronavirus? | Internet Society

Physical Retail Infrastructure

Macy has laid of 125,000 people in March alone and it has hundreds of thousands square feet of retail store and rental obligations which will draw down its coffers as the pandemic continues and people stay at home.

Supply Chain

The International Chamber of Shipping said the pandemic has cost the worldwide industry around $350 million per week. There are over 225,000 Americans working in the freight transportation industry, and the disruption has jeopardized over billions in wages for these workers. This is just the loss to the supply chain industry in an of itself, it doesn’t even include the way it has affected in the supply chain of food/clothing/electronics/health-aid. China has already metered the supply of PPE(personal protective equipment) to various countries and the closure of many of its factories has stifled some of the 80% of Fortune 1000 manufactures, think plastics, clothing, appliances, cars.

Retail

Google just recently release their COVID-19 Community Mobility Reports to provide insights into how movements across different areas have dropped due to the pandemic.

Restaurants

When restaurants shut down, its not just restaurant owners and their employees that gets affected but also affected are the grocery stores, the coffee producers, the fisherman, the butcher and the farmers.

Tourism is one of the biggest contributor to the F&B industry and the F&B industry employs over 7m people in the US alone! With the effect of pandemic predicted to last for the next 6-9 months that’s a loss of employment for probably 50% of the entire F&B staff and indirect loss of few more million people supporting the F&B industry i.e the truck drivers, the janitors, the pit stops operators.

The food and beverage operators in different airports in the US alone employs over 200K people who will be out of jobs soon and for the forseeable future as footfall and air travel decreases.

Box Office

The US Box Office April’s earning for 2019 was $1.3bn whereas for April 2020 is $1500 expect this to continue for the next 6-9 months, that’s a net loss of $10 bn.

As people stop going to the movies, movie studios would scramble to cut their budget and renegotiate contracts. So expect to see CGI producers, caterers serving food to crew and casts, sound artists, make-up artists, entire movie industry coming to a halt or wages heading towards the low end of the spectrum. There are over 220,000 Americans working in the film production industry and another 50,000 in the theaters.

Live Sports

The postponement or suspension of sports leagues like the NBA, NHL, XFL, and more have created a huge vacuum not just for the leagues and players, but also the wide-ranging ecosystem that has cropped up around them. FiveThirtyEight estimates that, since about 21% of the NBA season remained when games were halted, the league stands to lose $350 million-$450 million from ticket sales alone if those games are not played – and that does not even include lost playoff revenues.

Post Corona

A rise in food delivery and cloud kitchens as is already evident with Uber EATS revenue up by 50% even though it’s a tiny fraction of their total business, but since restaurants themselves will either go out of business, we will see a rise in cloud kitchens and take out joints for the next 12-18 months.

ESports will see a dramatic rise as will the rise of independent content creators, we’ll see a huge upsurge in high quality indie content from creators turning on their creative spirits due to the quarantine.

Expect to see major M&As as smart investors scoop out failing companies at discounts and either shedding the fat off or selling it for scraps. Uber & Lyft?

Startups Before And After

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance.”

When the stock market falls dramatically, the public market investments fall in value immediately. But private market investments don’t reflect the changing environment for a quarter or two because they require a manual valuation process

Over the last 5 years, VC funding in technology businesses has seen an exponential growth fueled by cheap sources of capital due to the reasons I discussed above. Driven by the growth in public markets, many large funds had slowly siphoned off their earnings from the public markets to private equity and venture capital.

Leaving aside Uber, Lyft and WeWork, over 64% of the tech companies that IPO’d in the last couple of years are unprofitable. When times are good, most humans are willing to pay an above market price for things that they don’t even need, but when times are bad, people think twice to buy even essentials. We’ve already seen over 51% decline in the prices of Uber and Lyft in the last two weeks, thats a notional loss of over $50BN. Uber’s valuation during its private round stood at $76BN. Valuations of major companies will take a massive hit as companies rush to raise bridge rounds for staying afloat.

Uninhibited spending on marketing, R&D and growth at all cost will see a decline. Most startups are already rebuilding their expense bases from ground up.

Companies Selling to SMB

Companies selling to SMB’s will see a sharp decline in their revenue and wouldn’t expect it come up anytime soon, as SMBs themselves are at a risk of extinction. Companies that will be most affected by it will be POS providers like Faire, VendHQ, Clover, Square and a few publicly listed ones.

Due to the rising number of unemployment and drop in wages, spending in non-essentials software and tools will take a large hit.

Companies Selling to Enterprise

Companies like Salesforce/Workaday or those that were selling to Fortune 1000 will see their revenue fall faster than the stock market as enterprises try to rebase their own Operational Expenses. CxOs of major companies wouldn’t be willing to try out the latest “No Code” solution or replace their legacy systems as they try to save their own companies from going extinct. Expect to see some series A/B CRM/Sales/LowCode to get either wiped out or cut their staff by 80% which is already happening.

Whereas, companies selling remote productivity suites like Zoom/Slack/Notion will continue enjoying their growth.

Consumer Tech & D2C Brands

Companies targeted towards consumers that depended on advertising will see a massive decline in their revenue with Snap and Facebook being hit the hardest for the foreseeable future whereas usage will actually rise as more people stay at home! Tiktok and HouseParty has already seen a huge upsurge in downloads in the last two weeks and the strain of massive usage because of Netflix/Zoom/Youtube is already getting felt by telecommunications operators around the world. D2C brands with their massive OPEX and burgeoning marketing spends like Casper and Native are already facing the heat whereas companies similar to Brandless went extinct right before the COVID19 hit the shores of US. Globally,

Edtech startups are AND will continue to have a gala time! And we’ll see an increasing number of healthcare and biotech companies crop up in the next few years with rapid succession.

Startups that survive will become anti-fragile and resilient!

Countries Will Increasingly Focus On Self-sufficiency & Nationalism

Many countries are considering substantial border restrictions and some have even taken drastic measures to shut down ports and imports. While there hasn’t been any indication that the coronavirus is being transmitted through consignments, hysteria will lead to tighter border controls and increased scrutinization of exports and imports.

It seems highly unlikely in this context that the world will return to the idea of mutually beneficial globalization that defined the early 21st century. And without the incentive to protect the shared gains from global economic integration, the architecture of global economic governance established in the 20th century will quickly atrophy. It will then take enormous self-discipline for political leaders to sustain international cooperation and not retreat into overt geopolitical competition. - Robin Niblett is the director and chief executive of Chatham House

As the world is suddenly waking up to the jolting realization of their extreme dependency on the global supply chain and the mounting geopolitical tensions limit America’s access to its normal supply chains and the lack of homegrown capacity in various product markets limits the government’s ability to respond nimbly to threats and especially China, major world economies will start to look for more resiliency within their own borders. In the years ahead, we’ll see a major push from all parties towards a combined effort for localization and incentives to bringing back production to their own geographies.

The coronavirus pandemic will create immense pressure on corporations to weigh the efficiency and costs/benefits of a globalized supply chain system against the robustness of a domestic-based supply chain. Switching to a more robust domestic supply chain would reduce dependence on an increasingly fractured global supply system.

Resurgence Of Government Backed Healthcare

Countries around the world are slowly waking up to realize how fragile their healthcare system had been and how unprepared they’re in dealing with a pandemic like COVID19. Globally, the national governments are taking measures to dramatically increase the capacity of their ER and equipments to deal with the crisis and once this is all over, healthcare system will continue to get better with increasing government oversight and collective effort by the private sector to innovate at a rapid scale.

Insurance companies are slated to increase their premiums drastically as huge swaths of their insured customer base will increasingly get affected by the virus. We’ll see an

Surveillance & Greater Government Oversight

Yuval Noah Harare on his piece in the Financial Times writes “in this time of crisis, we face two particularly important choices. The first is between totalitarian surveillance and citizen empowerment. The second is between nationalist isolation and global solidarity”. We’ll see a shift from the democratic and neoliberal push against increasing government oversight with tighter rules and under the skin surveillance by nations around the world in the name of protecting its citizen from another pandemic from occurring.

With the unprecedented speed in the development of surveillance technology, he hypothesizes a government that could demand every citizen to wear a biometric bracelet that monitors body temperature and heart rate 24 hours a day. This doesn’t seem as far fetching since companies like Google and Facebook already has the data of how people are moving and spending their time and with new electronic health trackers, this could be a reality too.

A Shift From USD / A Move Towards A More Stable Assets

- Gold backed currencies had their own advantage which when abolished led to a messy interdependencies

- Bitcoin will rise wuhoooo